Updated January 2026 with context on provincial tax policy and direct-to-consumer wine sales in Canada.

A reality check — and a roadmap forward

Each year, the State of the U.S. Wine Industry Report from Silicon Valley Bank (SVB) serves as a reality check for the global wine business. The 2026 report, authored by Rob McMillan, is especially important because it confirms what many wineries already feel on the ground:

The wine industry is no longer in a cyclical slowdown. It is in a structural reset.

Before looking specifically at British Columbia, it’s worth summarizing the most important takeaways from the SVB report itself.

Key Findings from the 2026 SVB Wine Industry Report

1. The downturn is real — but beginning to stabilize

SVB estimates that U.S. wine consumption declined again in 2025, falling to roughly 329 million cases, down from about 336 million in 2024. Industry revenue declined to approximately US$74.3 billion, down from US$75.5 billion the previous year.

The nuance matters: the rate of decline is slowing. SVB believes the steepest part of the downturn is behind us, with a bumpy bottom forming in 2027–2028, followed by modest growth. 2026, however, is not a year of recovery.

2. The industry is splitting into winners and losers

One of the strongest themes in the report is bifurcation.

- Top-quartile wineries are still growing, even in a shrinking market.

- Bottom-quartile wineries are seeing declining sales, excess inventory, margin compression, and rising debt.

The difference is not size or location — it is behaviour. Top performers are disciplined with inventory and pricing, focused on direct-to-consumer (DTC), clear about who their customer is, and hospitality-driven rather than volume-driven. Lower performers rely heavily on wholesale or walk-in traffic, discount broadly, and wait for demand to return instead of actively creating it.

SVB’s message is blunt: passive demand is gone.

3. Demographics are the real headwind

Oversupply matters, but demographics are the core challenge.

Baby Boomers — wine’s most reliable consumers — are drinking less. Millennials and Gen Z drink less alcohol overall, and wine is not their default choice. Consumption is more selective, value-driven, and occasion-based.

SVB points to the 30–45 age cohort as the next opportunity — but only if wineries adapt. Waiting for younger consumers to “grow into wine” the way previous generations did is no longer a viable strategy.

4. Oversupply is structural, not temporary

The industry remains overplanted and over-inventoried, even at the premium end. Grape contracts are being renegotiated or dropped, vineyard removals are increasing, and wholesale inventories remain bloated. Discounting — often hidden through private-label programs — is widespread.

SVB expects closures, vineyard removals, and exits to continue through 2026 as the industry right-sizes.

5. What actually works in 2026

Across top-performing wineries, SVB sees consistent patterns:

- Retention beats acquisition: Wine club retention is the strongest predictor of financial health

- Hospitality beats traffic: curated, personalized, appointment-based experiences outperform volume tastings

- Fewer SKUs perform better: focus and clarity win

- Digital amplifies — it doesn’t replace real relationships

Large events, broad discounting, and distributor-led selling without winery engagement are steadily losing effectiveness.

Update: Why Provincial Tax Policy May Decide Whether DTC Works in Canada

A central takeaway from the 2026 SVB Wine Industry Report is that direct-to-consumer (DTC) sales are no longer optional. With wholesale margins compressed and distribution increasingly selective, DTC remains one of the few channels wineries can control to protect both pricing and customer relationships.

In Canada, however, the effectiveness of DTC is shaped less by consumer demand than by provincial tax policy.

In January 2026, Wine Growers Canada and provincial wine associations from British Columbia, Ontario, and Nova Scotia released an open letter to Canada’s Premiers calling for reform to how DTC wine sales are taxed. This follows a July 2025 Memorandum of Understanding in which provinces committed to developing harmonized interprovincial DTC frameworks by May 2026 — a milestone intended to reduce internal trade barriers for Canadian wine.

The letter’s argument is straightforward: DTC transactions differ fundamentally from wholesale and retail sales. In a typical DTC purchase, consumers buy directly from a winery, applicable taxes are collected, age verification is completed, and a compliant product is shipped to the buyer. Provincial governments do not warehouse inventory, operate retail stores, or provide distribution services. Yet in many provinces, DTC shipments are still subject to markups, levies, and ad valorem taxes designed for systems that are not actually used.

This approach raises consumer prices, compresses winery margins, and limits the ability of small and mid-size producers to benefit from the very channel SVB identifies as critical for resilience.

Notably, workable alternatives already exist. British Columbia, along with Nova Scotia and Manitoba, has demonstrated that consumer protection and tax compliance can be achieved without wholesale-style markups on DTC shipments. Evidence suggests DTC primarily supports small-lot and winery-exclusive wines rather than displacing retail sales.

SVB’s global analysis highlights DTC as a key stabilizing force. In Canada, whether it fulfills that role will depend on how closely provincial tax policy aligns with the economic reality of direct sales.

What This Means for BC Wineries in 2026

The SVB report is U.S.-focused, but its implications for British Columbia are direct — and in many ways more urgent.

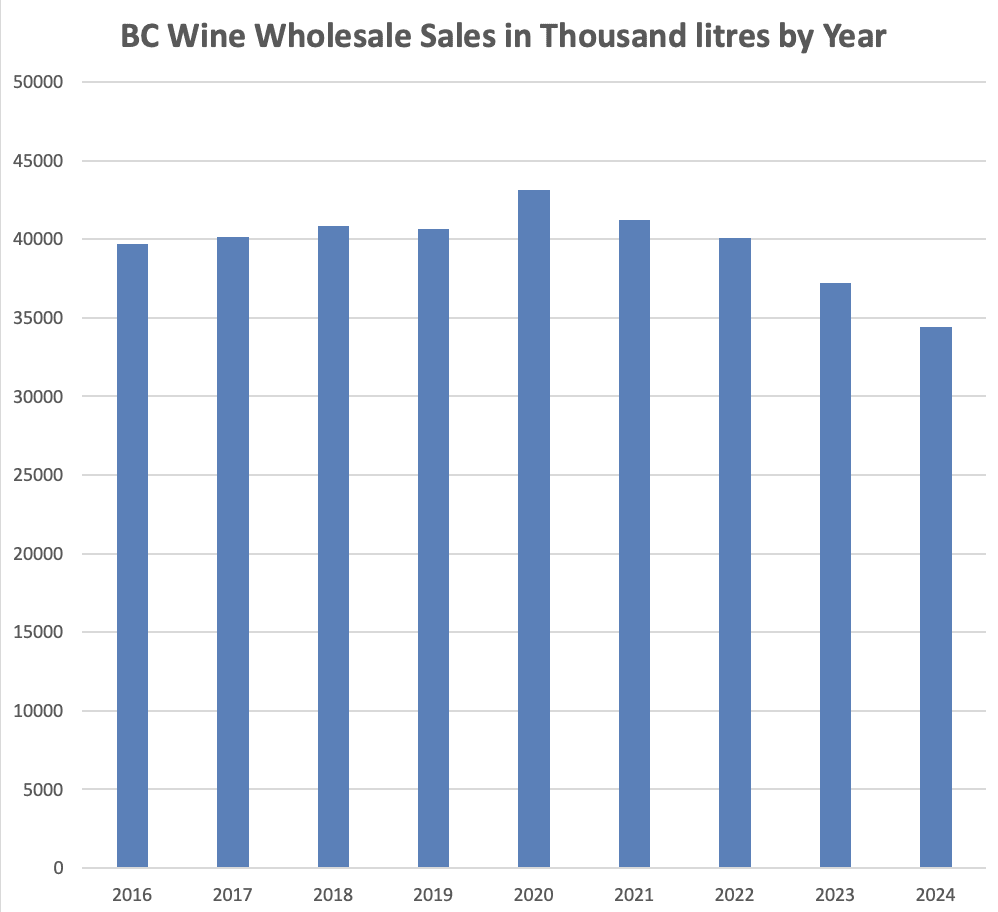

The chart below shows that BC wholesale wine sales volume is down roughly 20% from the 2020 peak.

The data shows that BC is not insulated from these trends — it is tracking them closely.

1. Same demand shift, less margin for error

BC wineries face the same demographic realities as their U.S. counterparts, but with a smaller domestic market, higher land and labour costs, limited export relief, and fewer options to quietly clear excess inventory.

Waiting is riskier in BC. Wineries that delay adaptation will feel pressure sooner.

2. “Buy BC” helps — but it isn’t a strategy

Local loyalty remains an advantage, but SVB makes one thing clear: goodwill does not replace relevance.

Tourism, patriotism, and protectionist sentiment can support sales, but they cannot compensate for unclear positioning, too many SKUs, weak club retention, or experiences that feel interchangeable.

Buy BC is a tailwind, not a business model.

3. A clear DTC lesson BC wineries should note

Two SVB charts are especially telling: regions with the highest DTC revenue share — notably Paso Robles and Santa Barbara — also show far more positive industry sentiment than many prestige-driven regions.

That alignment is not accidental. These regions focused early on accessible hospitality, appointment-based tastings, strong club cultures, and experiences designed around how people actually want to spend time with wine. The result was repeat visits, club memberships, and long-term loyalty.

For BC wineries, the takeaway is encouraging: high DTC performance is not about scale or prestige. It is about relevance, accessibility, and execution.

4. Pricing pressure is real, especially from $20–$35

This is a critical zone for BC. SVB shows long-term decline below $20 and softening demand even in the $20–$40 tier.

Price increases alone won’t protect margins. Clear hero wines matter more than broad portfolios, and consumers must understand why a wine is worth the price. As SVB notes, pricing must be part of a strategy — not the strategy.

5. Expect quiet exits and visible right-sizing

SVB expects 2026 to be a year of exits in the U.S. In BC, that likely translates to non-renewed grape contracts, vineyard removals, consolidation, increased bulk wine and Crafted in BC production, and fewer estate bottlings.

This right-sizing is already visible. A growing number of BC wineries are quietly testing the market, and you can see that trend reflected in this regularly updated list of BC wineries currently for sale:

👉 Do You Have $5M+ to Buy a BC Winery?

This is not a failure of BC wine — it is a correction to better align supply with real demand.

The Bottom Line for BC in 2026

2026 will not be a growth year. It will be a sorting year.

The SVB report is clear: growth will come back — but only for wineries that earn it.

For BC, 2026 is not about waiting for demand to return. It is about aligning production, pricing, hospitality, and storytelling with how consumers actually buy wine today.

Source: 2026 State of the U.S. Wine Industry Report, Silicon Valley Bank (SVB). Interpretation and analysis by BCWineTrends.